Seasonlity continued to tighten spreads and reduce the cat bond market's yield, but the discount margin is now back at September 2021 levels

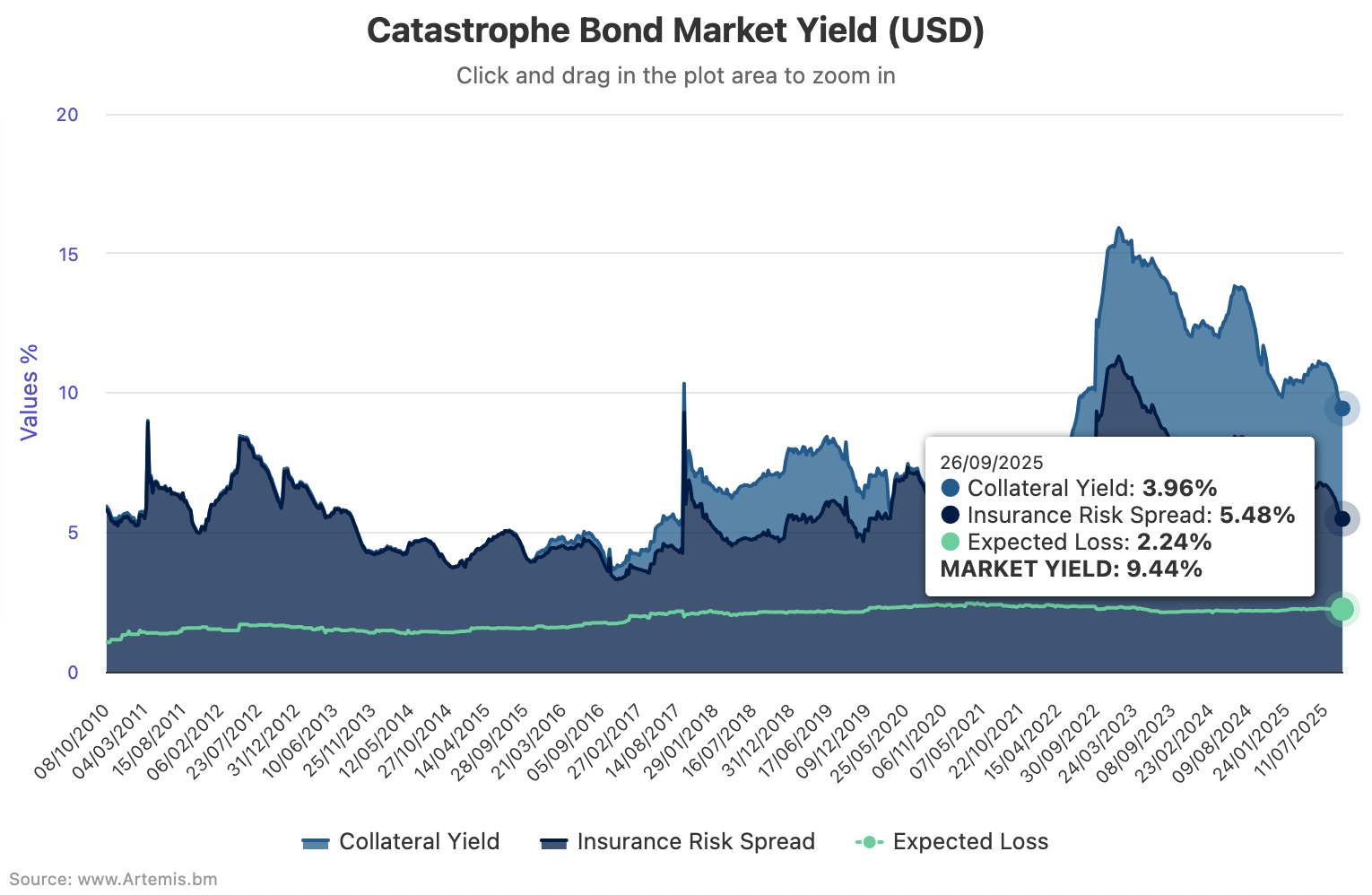

Cat bond risk spreads tighten to near 2021 levels | | | Cat bond market yield falls to 9.4% in September, risk spreads tighten to near 2021 levels  The overall yield of the catastrophe bond market declined further in September 2025, as seasonal spread tightening continued to be the major factor affecting that metric, with insurance risk spreads, or the cat bond market discount margin, now back at levels seen around the same stage of the year in 2021. The overall yield of the catastrophe bond market declined further in September 2025, as seasonal spread tightening continued to be the major factor affecting that metric, with insurance risk spreads, or the cat bond market discount margin, now back at levels seen around the same stage of the year in 2021. The insurance risk spread, or discount margin, fell to 5.48% at September 26th 2025, the lowest level since early January of 2022 and for an end of September figure it is now close to the level seen in 2021. Read the full story. Other articles: | | | | | | Please share this with colleagues and friends if you think they would like to receive it.

If you've been forwarded this but want to subscribe, visit Artemis.

| | | | | | You may be receiving this because you recently attended an industry event we partnered with, giving us permission to email you. If you don't want to receive our weekly ILS, catastrophe bond and reinsurance capital newsletter please Unsubscribe or Edit your subscription here .

© Steve Evans Ltd. - Artemis.bm

| | | |

No comments:

Post a Comment